Introduction

Kansas achieved a history of tax reform success throughout the 19th and 20th centuries, as evidenced by the dramatic evolution of Kansas’ code over the state’s 158-year history. The result is the current tax code, constructed primarily upon a relatively balanced three-legged stool of property, sales, and income taxes. While the majority of Kansans we met with are proud of the state’s three-legged tax structure, they also agreed that the time has come to build upon this structure and achieve lasting tax reform for the 21st century. The purpose of this book is to serve as a guide on Kansas’ path to tax reform.

In the course of producing the research for this book, we conducted dozens of interviews across the state, discussing tax reform options with hundreds of Kansans with an interest in tax reform. Several themes arose consistently in our meetings with citizens and stakeholders across Kansas. Those themes include an aspiration to make the state more competitive while ensuring stability, a willingness to learn from the past coupled with a desire to step forward into a better future, and a hunger for a thoughtful and comprehensive look at improving Kansas’ tax code. Kansans we met with carry a shared desire for a balanced conversation to achieve successful tax reform for the people and businesses that call Kansas home.

It is our goal to meet these demands with the work contained in this book, and by serving as an educational resource for the people of Kansas. We seek to apply the lessons of Kansas’ past, take a thoughtful and comprehensive look at Kansas’ tax code, and be a resource for modernizing Kansas’ tax code for the 21st century.

In the introductory text below, we summarize the recent history of Kansas’ tax changes and then lay out our objectives and guiding principles for thinking about tax reform. In the Executive Summary we list the building blocks with which Kansas can construct an enhanced, simplified, modernized tax code. The first two chapters of this book look at Kansas’ economy and budget. Chapters 3-7 build out the details to explain the building blocks of tax reform, with a view to creating structural improvements across the code over coming years.

Finally, we pledge to serve as a resource to lawmakers and stakeholders across Kansas as they fit and mortar together these building blocks into the architecture of comprehensive tax reform.

Synopsis of Kansas’ Recent Tax Changes

Few subjects are as fraught as is tax reform in Kansas. Unfortunately, “Kansas” has become a byword in many quarters, shorthand for the dramatic fight over what has been dubbed the “Kansas tax experiment” and its consequences. Although many of the tax changes adopted in 2012 and subsequent years have since been reversed, the issue remains fresh for many—and unresolved.

Some proponents of the 2012 tax changes feel that the efforts were cut short, or that tax changes were not allowed to proceed as intended. Many opponents feel that the reversals to date are incomplete. What cannot be disputed is that the past few years have been tumultuous, and that few policymakers would care to repeat that experience.

Kansas’ tax rate cuts that began in 2012 reduced revenues without commensurate reductions in expenditures to the point that the state struggled to meet its obligations. Reducing the tax wedge can certainly promote economic growth, but such growth is not sufficient to close the resulting revenue gap. Businesses became understandably wary about Kansas’ fiscal instability. When the state could neither meet its obligations within given revenues nor reduce expenditures in kind, it became inevitable that the tax changes begun in 2012 would be reversed, as they approximately were in 2017.

The tax debate that took course over the last several years is still raw for many Kansans.

The 2012 tax changes yielded uncertainty rather than greater competitiveness. The changes might well have kept business investment at bay, not because companies don’t like lower taxes—they do—or don’t have increased investment opportunities when tax burdens are lower—again, they do—but because they understood that the situation was unsustainable.

The 2012 tax changes were mostly focused on rates, not structure. The signature structural change from the 2012 law, the exemption of pass-through income from the individual income tax, was nonneutral in that it favored certain sorts of economic activity over others and created opportunities for tax arbitrage. Suddenly, a dentist’s income was likely to be tax-exempt, but her hygienist’s income was not. An independent consultant to corporations incurred no individual income tax liability in Kansas, but someone performing the same job responsibilities but as a corporate employee paid full freight.

The subsequent reversals were not particularly attentive to structural improvements either, focused as they were on fiscal sustainability. Retroactive tax rate increases were enacted to close the revenue gap. Policymakers pushing the rollback and rate increases were impelled by a sense of urgency, and doubtless believed that it was no time to undertake a broad tax study.

So why even consider tax reform?

Because, in short, addressing the structural inadequacies of Kansas’ tax code is now more important than ever. In recent years, Kansas policymakers have cut rates and they have raised them. They have created exemptions and repealed them. What they have not done is take a serious look at the actual scaffolding upon which the tax code is built and considered a plan to improve that scaffolding for a 21st century economy.

Now that the dust has begun to settle, the time has come to review the tax code, not with an eye either to slim or to grow revenues—the optimal revenue target is a policy choice outside the scope of this project—but to make sure that the state is raising the revenue it needs in the most neutral, efficient, transparent, and pro-growth way possible. It’s time to ask what’s working and what isn’t—to evaluate whether incentives are achieving their objectives, to identify ways to reduce compliance costs, and to better align the tax code to promote economic growth.

Furthermore, there is an issue at stake beyond simply reforming Kansas’ tax code. The Sunflower State’s brand will gain as much as its tax code from a successful tax reform. Kansans can come together, put the past behind them, and build a better future. The purpose of this book is to provide the tools and trajectory for the structure of Kansas’ tax code to be significantly improved. This book will address how those revenues should and should not be collected, and we leave it to Kansans to decide how much revenue should be collected.Our Purpose

To be clear: this is not a book about tax cuts. All else being equal, lower rates and lower tax burdens will incentivize investment and spur economic growth. However, the real world is complex, and all else is not always equal, in particular in a state that has undergone the significant tax and revenue changes Kansas has enacted since 2012. Regardless of how much revenue will be collected, Kansas can modernize the structure of its tax code to ensure that collections are made in a way that will encourage growth.

It’s time to turn the page on the debates of the past decade and chart a new course, one that makes Kansas a different kind of watchword. We are excited by the prospect that, a few years hence, “Kansas” will cease to be a word of warning and instead be a word that connotes reform and renewal. In recent years many states, including regional competitors like Iowa and Indiana, have modernized their tax codes to become more competitive and are enjoying the benefits of those reforms. It is time for Kansas to join their ranks. Wherever you stood in 2012 and wherever you are now, if you believe that Kansans deserve better than the state’s current tax code, this book is for you.

The following pages contain both an analysis of the state’s tax code and concrete recommendations for improving it. We will begin with the corporate tax code, given that the corporate tax is Kansas’ most inefficiently structured major tax, and therefore offers the greatest opportunity for reform and renewal.

We hope that you will find yourself agreeing with many of the recommendations in this book, but perhaps you will disagree with a few of them as well. We are eager to begin a robust and bipartisan conversation about modernizing Kansas’ tax code to suit a 21st century economy. Imagine a world where people talk about the lessons learned in Kansas that illuminated the path to Kansas’ modernized tax code and reinvigorated future. We’re imagining it. We invite you to join us.

A Menu of Tax Reform Solutions

Corporate Income Tax

Kansas’ income tax is functionally a two-rate tax, with most corporate income taxed at 7 percent. Some firms face little or no liability under the corporate income tax, but for others, structural deficiencies in the state’s approach to corporate taxation can lead to uncompetitive burdens and penalize in-state investment. Our recommendations would create a more neutral corporate tax environment which encourages long-term investment in the state.

Removing International Income from the Tax Base. Inaction on the part of policymakers has Kansas poised to tax international income, with corporations potentially facing significant in-state liability for the activities of their foreign subsidiaries or related corporations, which would make Kansas far less attractive to multinational corporations. Lawmakers should reaffirm the state’s traditional position (in line with other states) of not taxing international income.

Locking in Full Expensing of Capital Investment. Commendably, Kansas conforms to the new federal policy of allowing corporations to fully deduct the cost of their machinery and equipment purchases in the first year. But with the current federal treatment scheduled to expire, Kansas would be well-advised to lock in the current system, decoupling from future changes to federal law and instead providing permanent full expensing.

Repealing the Throwback Rule. Kansas’ throwback rule punishes businesses that sell out of state, encouraging them to relocate to—or at least locate distribution facilities in—other states. With studies suggesting that, over time, tax avoidance strategies eliminate most or all revenue gains from throwback rules, repealing the throwback rule would be a sound investment in Kansas’ economy.

Shifting to Market Sourcing of Service Income. Kansas’ tax code treats companies more favorably when they produce and sell tangible goods than when they sell services or other intangibles. This distinction lacks economic justification and should be eliminated.

Conforming to Federal Treatment of Net Operating Losses. Federal law now provides for unlimited net operating loss carryforwards, capped at 80 percent of tax liability in any given year, while Kansas offers a relatively stingy 10-year carryforward. Policymakers might consider increasing the length of the carryforward period, or, alternatively, conforming to federal treatment for simplicity’s sake.

Reviewing Business Tax Incentives. A growing number of states have established panels, commissions, or ad hoc committees to review tax incentives periodically. With a new tax incentives database in the works, policymakers should formalize a regular evaluation process to assess the return on investment from the state’s economic development incentives.

Individual Income Tax

Kansas’ individual income tax is in the middle of the pack for rates and collections, but opportunities exist for structural improvements affecting individuals and pass-through businesses. The state’s failure to respond to changes in the federal tax code, moreover, yields higher taxes on many Kansans, an unlegislated and nonneutral tax increase that policymakers may wish to address. Our recommendations are focused on creating a more regionally competitive individual income tax.

Indexing Income Tax Provisions for Inflation. To avoid bracket creep, where inflation leads to greater income tax liability even when real income remains constant, Kansas should index the major provisions of its individual income tax—the brackets, standard deduction, and personal exemption—to inflation.

Enhancing the Standard Deduction. Because it is not inflation-indexed, Kansas’ $3,000 standard deduction has lost half its value since it was created in 1988, an erosion even more notable now that the federal standard deduction stands at $12,400. Kansas also offers both marriage bonuses and penalties in its standard deduction, with a joint filer deduction of $7,500 (more than double the single filer deduction), but a $700 per person or $850 per couple additional deduction for senior citizens. Kansas policymakers should consider increasing the standard deduction and eliminating these bonuses and penalties.

Allowing an Independent Choice of Itemization. Under the new federal tax law, far more taxpayers find it advantageous to take the more generous federal standard deduction than to itemize, but this decision currently increases their Kansas tax liability, creating an unlegislated tax increase. Kansans should be allowed to itemize on their state return even if they claim the standard deduction on their federal return.

Rolling Back Excessive Credits. Some of Kansas’ tax incentives are barely claimed at all, and others fall far short of their objectives, but they create administrative costs by their mere existence. While individual income tax credits only carve out the tax base slightly, a cleanup of the existing credit structure is appropriate.

Eliminating the Social Security Tax Cliff. Kansas excludes Social Security from the taxable income of those whose federal adjusted gross income is $75,000 or under, but taxes it in full once a taxpayer earns a single additional dollar. Policymakers should explore the implantation of a gradual phaseout of the benefit to avoid this steep tax cliff.

State and Local Sales Taxes

Kansas’ sales tax is imposed on a narrow base that exempts many goods and most services, a holdover from an earlier era, while the state’s approach to remote sales tax collections raises serious legal questions and imposes significant compliance costs. Our proposals would simplify and modernize the sales tax, bringing it in line with today’s economy.

Broadening the Sales Tax Base. A well-structured sales tax applies to all final consumer purchases, both goods and services, while exempting business inputs. Kansas’ sales tax falls far short of this goal, and in an increasingly service-oriented economy, it erodes further each year. We offer a menu of base-broadening options to enhance the stability of the sales tax and generate additional revenue that could be used to reduce the sales tax rate or pay down reforms elsewhere.

Excluding Business Inputs. Kansas policymakers have long recognized the importance of excluding business inputs from the sales tax base to avoid pyramiding, but little progress has been made in expanding the scope of these important exemptions. Policymakers should consider exemption certificates and the adoption of better definitions of business inputs to reduce the impact of this hidden tax.

Removing Barriers to Interstate Commerce. Nearly all states have responded to their newfound authority to require collection and remittance of tax on remote sales, but Kansas is alone in imposing these requirements without a safe harbor for small sellers, which is likely unconstitutional. Policymakers should enact legislation providing such a safe harbor, disavowing retroactive collections, providing clear statutory language regarding marketplace facilitators, and eliminating its legally dubious click-through and affiliate nexus provisions.

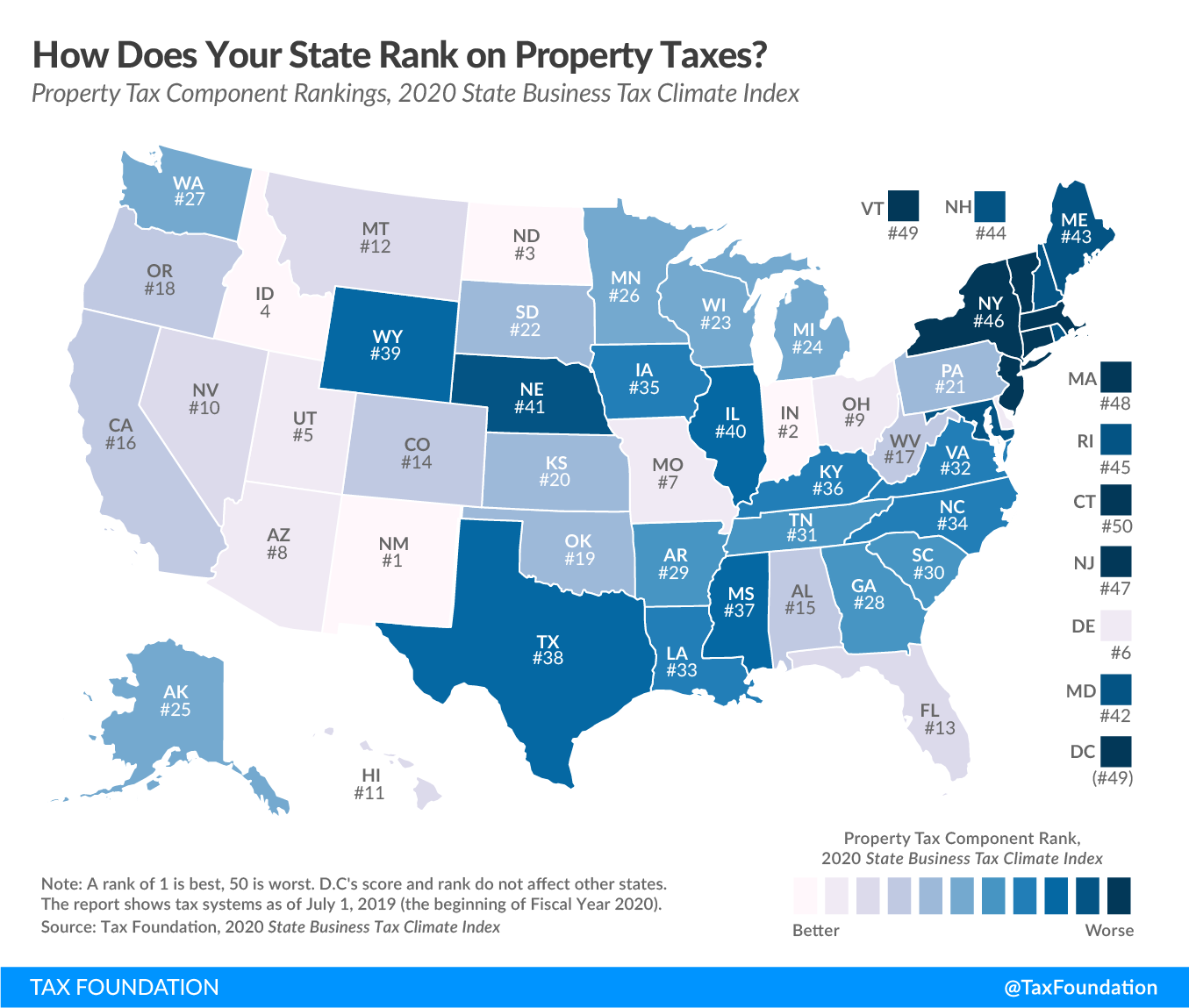

Property and Related Taxes

Kansas’ property tax ranks above average in its structure, and the state has a laudable system of property tax administration. Further improvements can be made that will benefit homeowners and businesses. Property tax controls can be improved to increase transparency and taxpayer involvement in the process of increasing property taxes. The property tax base should be focused on land and its improvements, insofar as possible, and the administration of property taxation for retail properties should be improved. Finally, Kansans should thoughtfully study and consider options for consolidating local governments.

Restructure Property Tax Lid in the Mold of Utah’s “Truth in Taxation” Requirements. Kansas passed a property tax lid into law in 2015. It took effect in 2017. The lid has caused dissatisfaction with both local government officials and advocates of property tax restraints. Kansans can restructure this lid in the mold of Utah’s Truth in Taxation law, creating a property tax cap system that thoroughly informs and engages property owners in any decision to increase property taxes while not unduly constraining local governments.

Reduce Reliance on Tangible Personal Property Taxes with Potential Offsets. Kansas’ taxation of tangible personal property is a nonneutral and inefficient part of its property tax code. Kansas has recently moved to exempt various forms of business tangible personal property from taxation and should continue to move forward in removing all tangible personal property from the tax code, thus circumscribing the property tax to land and its improvements.

Preempt Local Governments on Taxation of Gross Earnings from Intangible Property. The local taxation of earnings from intangible personal property is one of the more peculiar and anachronistic provisions of Kansas’ property tax code. This tax is levied by a small share of local governments. The state legislature should preempt the taxation of earnings from intangible personal property.

Direct County Appraisers on Proper Methodologies for Appraising Big-Box Retail Properties. The volatile appraisals of big box retail properties cause instability for both businesses and local governments. However, the Kansas Board of Tax Appeals and Supreme Court have consistently ruled that retail properties should be appraised on the value of their land and improvements, and that appraisal formulae should not be based upon the income-potential or lease-potential of a retail property. The Director of the Division of Property Valuation should thus provide clear guidance to county appraisers for valuing big-box retail properties.

Revisit the Requirement for Partial Payment of Tax that Is under Appeal. Kansas can also reconsider the requirement for the payment of the disputed portion of a tax that is under appeal. This change would improve Kansas’ property tax administration, and if structured properly, reduce volatility for local government finances that is the result of disputed appraisals.

Study and Consider Ways to Achieve Local Government Consolidation. Kansas should formalize an effort to study the need for local government consolidation and consider options for the same. Local government consolidation frequently arose in our discussion of property taxes across the state. However, such changes require a careful, well-thought analysis of where opportunities exist to improve the efficiency of local governance through consolidation.

Other Tax and Revenue Considerations

Although income, sales, and property taxes make up the bulk of state and local taxes in Kansas, other taxes (like excise and severance taxes), as well as revenue- and budget-related provisions like the Budget Stabilization Fund, merit consideration. Our recommendations promote certainty and stability for the state and taxpayers alike.

Shoring up the Rainy Day Fund. Kansas was one of the last states to implement a rainy day fund, with the 2016 enactment of legislation creating the Budget Stabilization Fund. Currently, however, deposits are only required for a few years, the calculation of mandatory deposits is fairly arbitrary, there are no specifications of when funds may be withdrawn, and there is no replenishment provision for when a withdrawal has been made. If the rainy day fund is to provide a buffer in the next recession, policymakers must establish it on a firmer basis.

Maintaining the “Border War” Truce. Kansas and Missouri recently implemented a ceasefire in the “border wars” in which both sides offered incentives to lure companies back and forth across the border dividing Kansas City, Kansas from Kansas City, Missouri. This truce is not binding on localities, however, so policymakers should do what is in their power to encourage or induce local governments not to defect.

Above is a brief excerpt from Kansas Tax Modernization: A Framework for Stable, Fair, Pro-Growth Reform. To download our full reform guide, click the link below.

Download The Full Book

Stay Informed on Tax Policy Research and Analysis